When it comes to investing, it’s easy to focus on day-to-day headlines and market moves. But the true power of investing can be found outside of those headlines, in mathematical concepts and historical data.

Of course, we still stay at the frontlines of research, trading, and market analysis when it comes to managing client investments. But we also want to illustrate the power of a few basic concepts that are central to your overall financial plan.

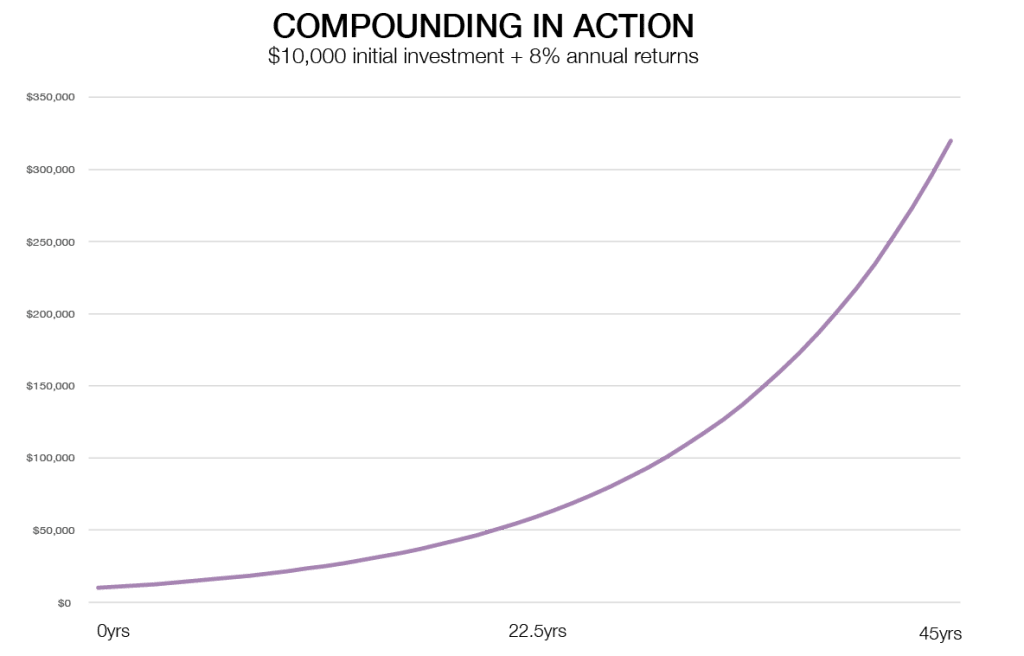

The power of compounding

Compounding is the reason you might put $10,000 in a retirement account at age 25, then retire with more than $300,000 less than 50 years later — even if you never invested another dime of new principal

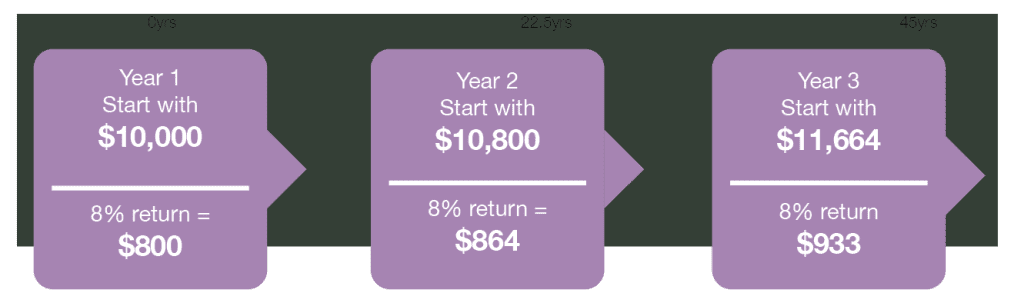

This kind of exponential growth happens when your returns begin to generate returns of their own. The first year the $10,000 is invested, an 8% return would generate $800. The second year would start with $10,800 invested; an 8% return on that is $864. The returns from the first year generated that final $64 in year two. In the third year, the starting amount would $11,664, so an 8% return would generate $933 and so on through the years

The power of habit: dollar-cost averaging

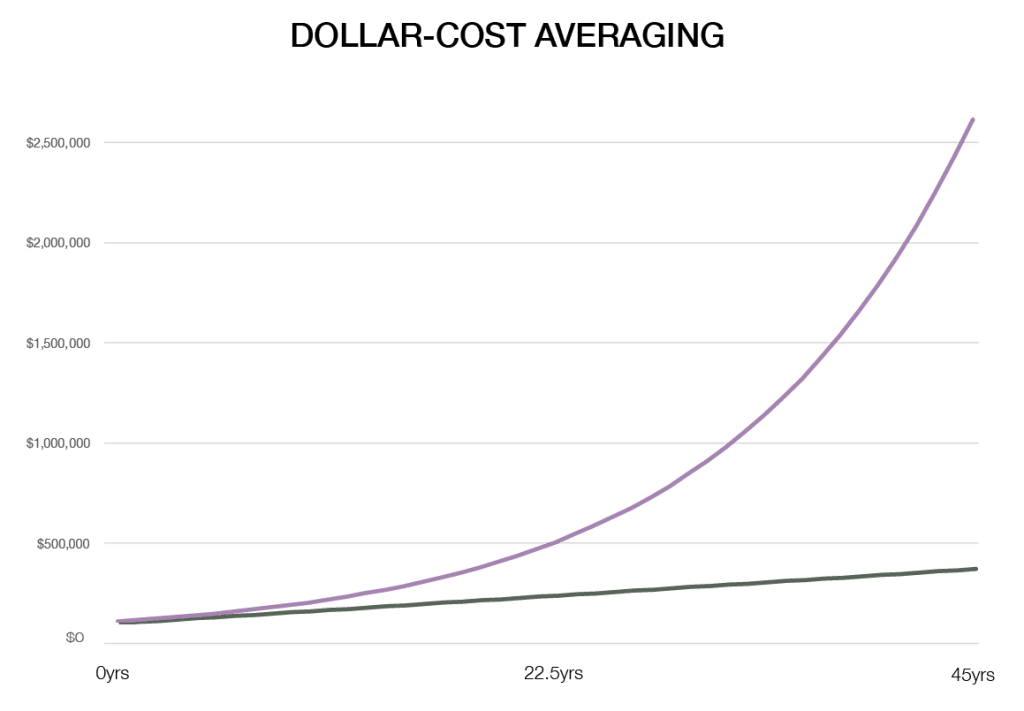

Compounding gets even more powerful when we add in something called dollar-cost averaging. While the first chart helps illustrate compounding, it’s rare for someone to invest $10,000 then leave it untouched. Instead, people tend to invest smaller amounts throughout their lives. Instead of a $10,000 initial investment, consider a $6,000 investment to start, then $6,000 per year ($500 per month) for the next 45 years. That’s called dollar-cost averaging, in reference to the idea that you’re investing regardless of whether markets are up or down.

The green line represents this basic idea and shows only the principal investment.

As you can see, the power of habit helps grow the principal investment from $6,000 to more than a quarter million.

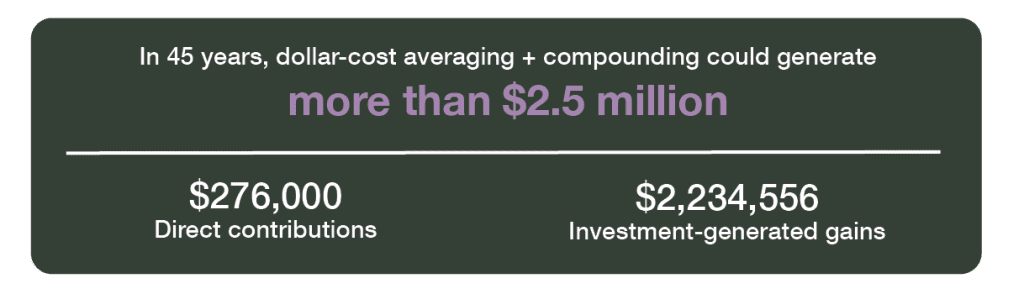

The purple line shows what happens when investing and compounding are added to the mix. Assuming an 8% rate of return, that dollar-cost averaging strategy could turn into more than $2.5 million in 45 years.

The vast majority of that sum — more than $2 million of it — came from returns generating returns of their own.

Time in the market over timing the market

So far, we’ve been using annual returns of 8% — the historical average for the stock market. But the stock market doesn’t return 8% each year; that’s just an average. In reality, those returns fluctuate, which can affect more than just overall returns and the math behind compounding.

Fluctuating returns tend to trigger the emotional component of investing, especially when investments lose money. Humans are programmed to avoid risk and chase reward, and this can create a temptation to time the market.

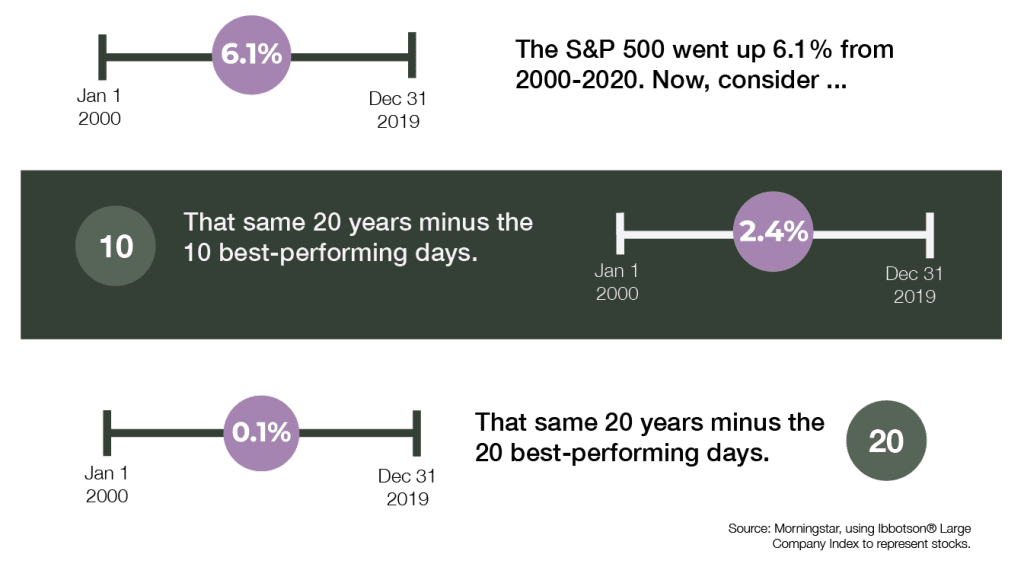

Exiting the market can be risky, though, as you may miss top-performing market days, which can impact potential returns significantly. Consider the 20-year period from January 1, 2000, through the end of 2019. Over that period, a sample index of large stocks returned 6.1% on average. If you missed just the 10 best-performing days that number falls to 2.4%. Miss the 20 best-performing days, and the number falls to 0.1%

Staying invested can be as important as your initial investment when it comes to leveraging concepts like compounding and dollar-cost averaging; it’s a major reason we emphasize long-term goals over daily market fluctuations.

While we adjust our investing strategies based on market conditions, we also apply these fundamental truths about investing to our financial plans. We are always happy to discuss these concepts in more detail, including how they relate to your plan specifically.

Remember: All investing involves risk, including loss of principal. We use an 8% average rate of return for the stock market, which is in line with historical averages, but all examples in this article are intended to be illustrative and educational in nature. Past performance does not predict future results.