If you want to become a successful investor, there’s one “rule” to follow: Buy low, sell high. Of course, this is far easier said than done. In fact, trying to follow this rule—known as timing the market—can famously derail even the best investing strategy.

That doesn’t mean you should abandon the goal to buy low and sell high, however. Rather, you probably want to try a different approach: Dollar cost averaging.

What is dollar cost averaging?

Dollar cost averaging refers to regular, consistent contributions to an investment account. For instance, if you set up automatic contributions to your retirement account, you’re likely investing (buying) every time you get paid.

Because these purchases happen any time you’re paid, regardless of what the market is doing, you may be just as likely to buy low as you are to buy high.

For instance, when the market falls, many investors get nervous and want to sell their investments. Others suggest “buying the dip” to take advantage of a potential rebound. If you’re contributing automatically, you end up buying whether the selloff turns out to be a dip or part of a broader market trend.

This consistency can help boost returns over time.

Consistency and performance

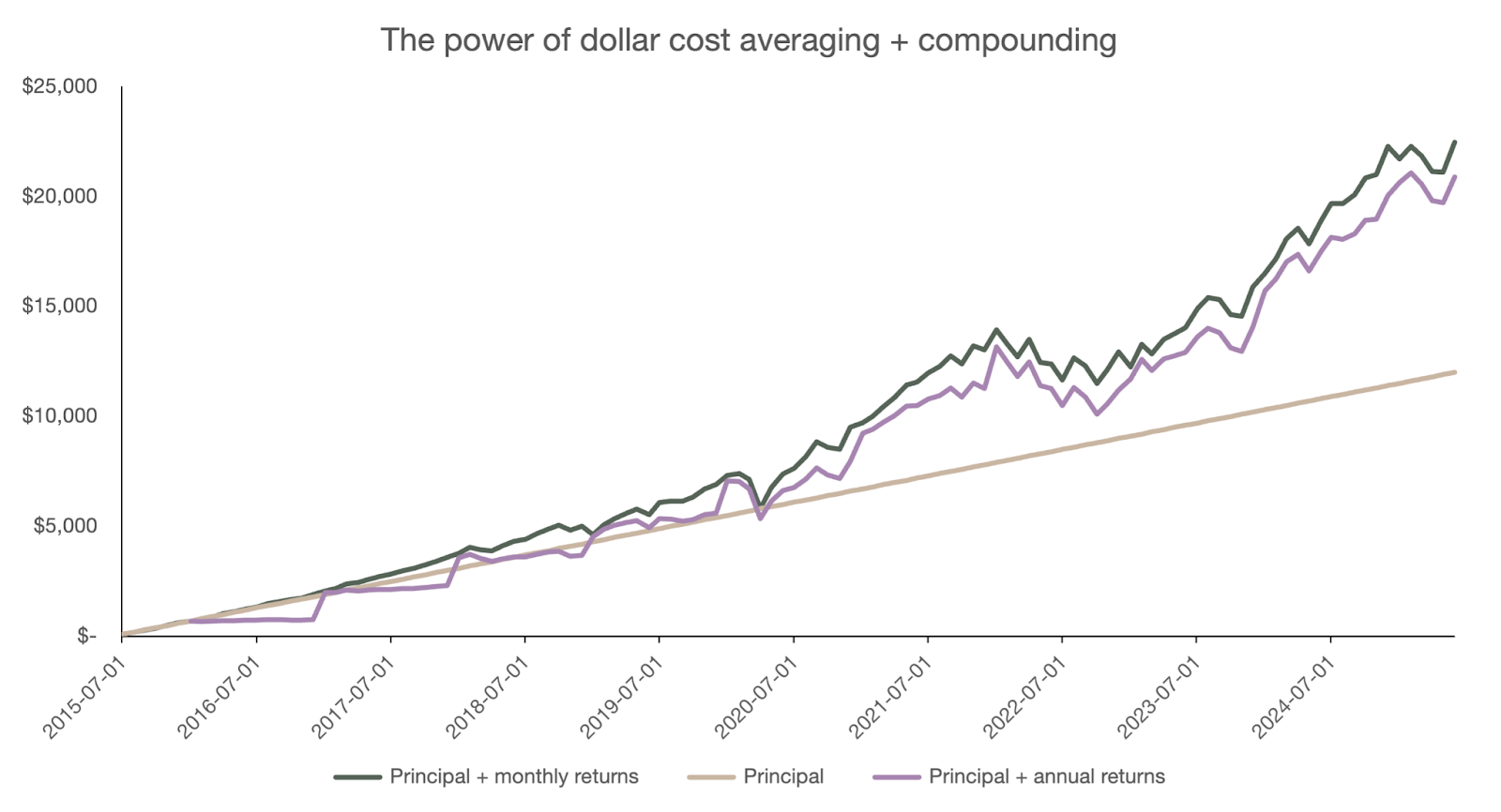

To understand how this works, let’s consider an example. Say you decided to start investing 10 years ago, in July 2015. You decide to budget $100 per month towards saving and investing.

The beige line shows what happens if you simply put the $100 per month into a savings account with negligible interest. While you’d save $12,000, keeping those funds in cash isn’t the best use of your savings; inflation would eat away at the value and you’re missing out on the potential for investment growth.

Let’s consider a second example—one where you invest your savings once a year. We’ll use the same controls—setting aside $100 a month—but in this example, you’d wait until January 2017 to invest the first $700 you’d set aside. That money is invested in the S&P 500 returning roughly 1% for the year.* In January 2018, you invest another $1,200… and continue the trend each January through 2025.

That’s the purple line. As of June 2025, you’d have more than $20,800.

Now consider what happens if, instead of investing once a year, you had invested the $100 you set aside every month, instead of waiting until January. This small adjustment is represented by the green line. You’d have more than $22,400 in June 2025—8% more, simply from applying dollar cost averaging.

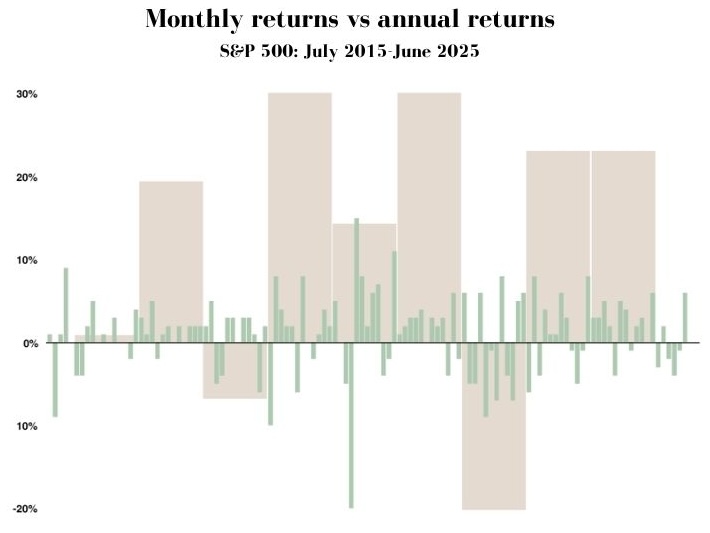

Why the increase in returns? Simply put, buying every month—or dollar cost averaging—increases your chances to buy low. There’s more ups and downs in the market in the short term than in the long term. Consider how monthly returns compared to annual returns during the period in question.

The takeaway? Automating your retirement contributions might not seem like a savvy way to “game” the market, but it’s a great way to implement a “buy low, sell high” mentality without adding the additional risk that often comes with trying to time the market.

If you have questions about dollar cost averaging or your investment strategy overall, please reach out to discuss.

*We used S&P 500 index returns (data provided by S&P Dow Jones, LLC via the St. Louis Federal Reserve) for this example. However, you cannot invest directly in a stock market index such as the S&P 500. Funds that track the S&P 500 charge fees that impact performance, meaning actual returns, even for indexes that track the S&P 500, may vary slightly from these numbers. The examples in this article are meant to be educational in nature. Past market performance does not predict future performance, and individual investment returns may vary.