When it comes to managing investments, diversification is at the heart of what we do. Each type of investment serves a different role in a portfolio, just like ingredients in a recipe. Combining investments in different ways creates opportunities for potential returns or to manage risk.

Given how important diversification is to how we help you invest, we want to spend some time going over how it works, both in theory and in practice.

What are asset classes?

Groupings of investments — stocks, bonds, cash, real estate, commodities — are known as asset classes. Each asset class serves a purpose — they all have desired benefits and clear risks.

In general, the goal of investing in stocks is growth. On average, the stock market returns roughly 7% per year, which is more than bonds.

In general, the goal of investing in bonds is capital preservation and risk management. U.S. Treasuries are the staple of most bond portfolios, including ours, and the U.S. government has never defaulted on its debt. (It’s important to note that bonds can still lose money, but unless the issuer defaults, these investments don’t tend to drop as dramatically as stocks do on occasion.)

Cash is often considered a safety play but is subject to inflation risk. The good news is a number of other asset classes may provide some protection against inflation.

Real estate may be useful as an inflation hedge since overall values (and rent, if you are renting the properties) tend to increase along with other consumer prices. Commodity prices also tend to increase along with inflation. Beyond that, how commodities are valued varies significantly based on industry, meaning they can be highly uncorrelated to other investments. (For instance, oil prices may jump significantly while wheat prices fall, or vice versa.)

Can you diversify within asset classes?

It’s possible to go a layer deeper within asset classes, as well. With stocks, you have categories, like growth or trend (which look to be increasing in value), income or dividend (which pay a yield to shareholders), and value (stocks that look to be trading at a lower price than they may be worth, based on fundamentals). You can also group stocks according to their industry, or sector: technology, financials, utilities, and so on.

For bonds, you can categorize them by issuer, for instance the government or corporations. You could also categorize bonds by risk-level: investment grade or high-risk.

When you’re building a portfolio of investments, it’s important to make sure there’s enough diversity among your investments. The term diverse has the same meaning in investing as it does elsewhere: It simply refers to variety. A truly diverse portfolio is invested across asset classes and also holds diverse investments within those asset classes. Let’s take a closer look.

How does diversification work?

At the highest level, you want to invest in a wide variety of asset classes. That means it’s better to invest in both stocks and bonds than to invest in stocks alone.

There’s a reason for this. Stocks and bonds perform differently — they react differently to various events and stimuli. In market speak, their performance isn’t correlated. That means if there’s a big dip in the stock market, having part of your portfolio in bonds can help protect you from that dip.

It’s worth noting, however, that the logic around the correlation between stocks and bonds is evolving. In the past, bonds tended to react differently than stocks in many instances. These days, however, it’s not uncommon for a correction in stocks to be accompanied by a correction in bonds. The reasons behind this are fairly technical in nature, so we won’t get into them. But this relationship between stocks and bonds is one of the reasons we use mathematical models and analysis to help ensure we’re finding assets that truly react differently, to the best of our ability.

One of the ways we do this is by making sure we have diversity within each asset class.

Take stocks as an example. If someone in the 90s was invested primarily in tech stocks, they would have been hit hard when the dot-come bubble burst in 2000. If that same person had also invested in banks, retailers, pharmaceutical companies, and energy stocks, in addition to tech stocks, they may have seen their investments lose value, but probably not to the same degree as a tech-only portfolio.

One way we apply this thinking is using trend stocks and value stocks. We want to make sure that when the stocks are increasing in value, you’re invested in the companies that are trending upward. We also want to make sure you’re invested in stocks that are fundamentally sound, and perhaps trading at a discount. When markets fall, investors tend to sell trend stocks and buy value stocks. So the value portion of your stock holdings may act as a hedge in these situations.

Building a diversified portfolio

The good thing about diversification is that a little bit goes a long way. In fact, research shows that after a certain point, the benefit of adding new types of investments starts to diminish.

The best way to diversify is to find assets that are not correlated, like our earlier example of stocks and bonds. Financial analysts often look at historical performance for different assets to find out how correlated they are to each other.

Financial advisors tend to use this type of analysis and research to make sure you’re invested in a handful of assets with low correlations.

According to one study by investment firm MorningStar, going from one type of investment to four different types of investments can reduce volatility in a portfolio by 50%. Volatility refers to big swings up and down, so less volatility can help with managing risk.

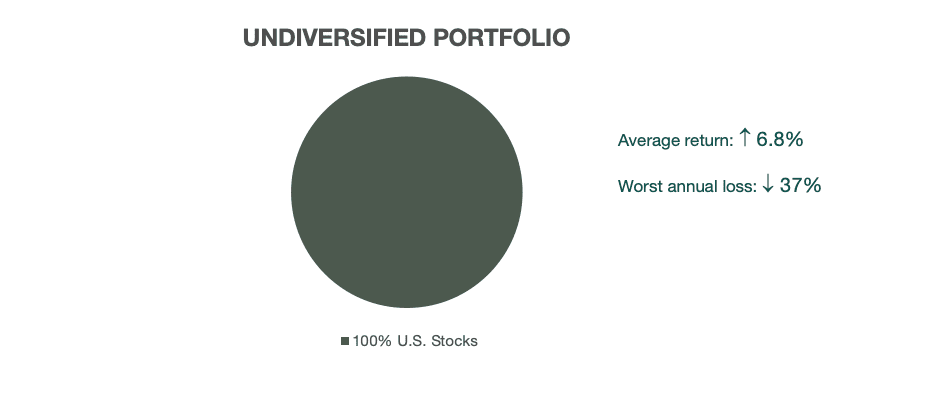

For instance, take a look at the chart below. If you were invested in only U.S. stocks from 1998 to 2018, your money would have returned just under 7% on average. But, for one calendar year, your portfolio was down 37%, which is hard for any investor to stomach.

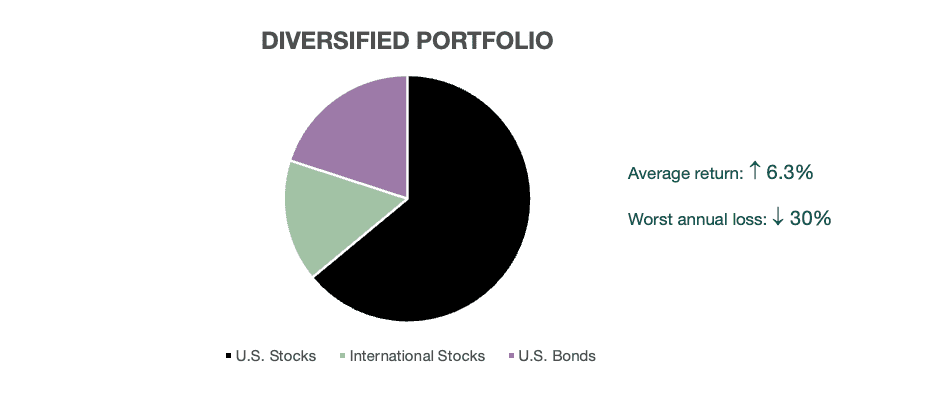

Now, imagine that same time period but with a diversified portfolio: 20% in U.S. bonds, and 16% in international stocks. The rest (64% ) are in U.S. stocks. By adding this diversification, your worst year is now a loss of 30% — still significant but less jarring than 37%. Meanwhile, you haven’t compromised too much on returns.

Source: MorningStar

When determining how to diversify assets, advisors essentially use a version of the table above. The precise metrics vary and tend to be more complex, but the idea is the same. The goal is to get you the highest possible return with the lowest possible “worst annual year.”

That’s also one of the reasons we adjust asset allocations based on market conditions. A different “mix” of diverse investments may be more appropriate in certain market conditions than others. Using math and data to help inform those decisions helps us take advantage of the potential benefits of diversification through a more objective lens.

Hopefully, the information in this article helps add some context to our monthly market updates, and as always, if you have questions about how diversification applies to your portfolio specifically, please don’t hesitate to ask.