Setting you up for success in retirement is one of the biggest parts of our job at Revo Financial. While we start with saving and investing, that’s just the beginning of retirement planning. There’s also a great deal of strategy involved in how you tap into your nest egg.

As you near retirement and begin thinking about where your income will come from, it’s important to understand a concept known as sequence risk (or sequencing for short). This concept is a big part of any withdrawal strategy in retirement.

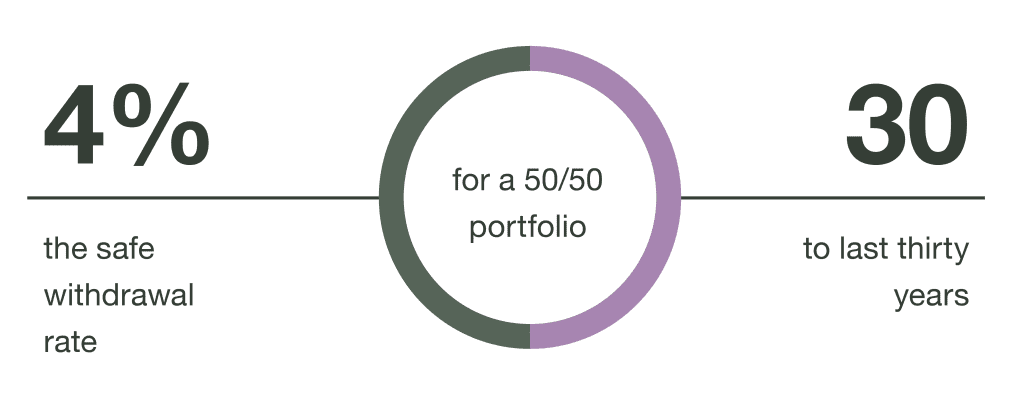

Money in, money out

Historically, the stock market returns roughly 8% annually. Because of that, many people think they can withdraw 8% of their investments each year in retirement. In reality, that number is much lower: 4%.

Not only that, most of us think about our income in dollar amounts, not as percentages. So, while 4% is the safe number, it’s not always practical in terms of planning. Withdraw 4% from a $1 million portfolio, and you have $40,000. The next year, however, you’d be taking 4% out of $960,000, which is $38,400 — a pay cut.

Of course, that example assumes no returns on the $960,000. With positive returns, you may see a raise, but with negative returns, you’d likely see an even bigger drop in income.

That, in a nutshell, is why it’s so important to stay invested during retirement, and why we keep a portion of retiree portfolios invested in stocks and focused on growth. It’s also why we need to be strategic about income planning in retirement.

Timing matters

It’s nearly impossible to time exactly when to buy or sell an investment, but that doesn’t mean timing isn’t important. Specifically, the sequence of returns during your retirement (which years are up and which are down) plays an important role in how long your money might last.

When investments lose money early in retirement, withdrawing money essentially locks in those losses. That can be hard to recover from, especially in retirement when we need to focus your portfolio on capital preservation along with potential growth.

Consider the following scenarios. At left, we have the actual returns for the S&P 500® from January 1, 2005 through 2024. At right, we have those same returns in reverse chronological order, starting with 2024 and going back through 2005. In both cases, the average rate of return is just under 12%, and in both cases we assume a starting balance of $500,000 and a yearly withdrawal of $30,000. As you can see, despite all other factors being equal, the order of good performing years versus bad makes a big difference—more than a million dollars worth.

The takeaway? Poor market performance early on in retirement can have an outsized impact on your money and how long it will last.

What this means for planning

There are a few ways we take this into account when working with clients. First, we want to make sure you have a diversified income stream in retirement. There may be years where we don’t want to withdraw money from your portfolio, aside from the minimum distributions required by the IRS. If that’s the case, we’ll look at where else you might find income. This could be via products, like an annuity, or via part-time work. There’s also Social Security or more liquid savings.

(It’s worth noting that working part time in retirement is something we encourage from a lifestyle perspective, too, as it can help you stay engaged and prevent boredom over time.)

It’s also a reason we keep client portfolios diversified in retirement. While we shift the focus of your investments to income generation, we keep a portion of your money focused on growth, usually through investments in stocks (versus bonds).

A few things to remember in addition to what we covered here:

- It’s impossible to predict how long you’ll need this money to last, and we’re hoping it’s a long time.

- Expenses tend to increase in retirement (particularly medical expenses). That, combined with increasing costs of living, means you may need to increase the dollar amounts of your withdrawals periodically.

- Alternative investments into things like commodities can help protect against these inflation risks as part of a diversified portfolio.

These are all factors we plan for when managing your investments and updating your financial plan. Expect these themes and discussions to come up as we move toward, and through, your retirement. If you have any questions about what we covered in this article or want to discuss your own retirement income plan, we are happy to discuss.

Remember: All investing involves risk, including loss of principal. All examples are intended to be illustrative and educational in nature. Past performance does not predict future results.